阿摩線上測驗

阿摩線上測驗

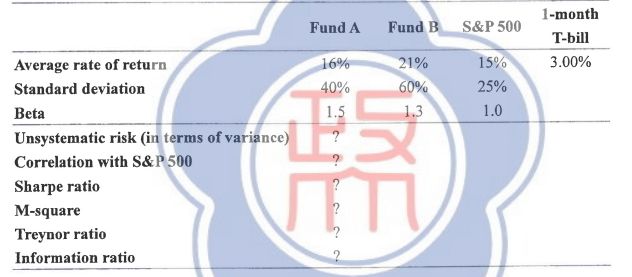

題組內容

4.The risk-free rate, average returns, standard deviations, and betas for Fund A, Fund B, the S&P 500 Index, and 1-month T-bill are provided. If we use the variance as a proxy of the total risk, the unsystematic risk can be obtained by subtracting the systematic risk from the total risk.