阿摩線上測驗

阿摩線上測驗

題組內容

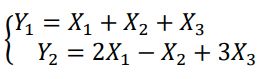

4. Let X1, X2, X3 be i.i.d. (independent and identically distributed) random variables with mean

0, 2, -1, and variance 1, 4, 9, respectively. Let Y1, Y2 be some linear combinations of X1, X2, and X3 as

follows:

For the sake of analysis, we set

(2) (8%) Find the variance-covariance matrix of